What Is General Ledger Reconciliation Explained Simply

Struggling with what is general ledger reconciliation? This guide breaks down the process, its importance, and how automation makes it easier than ever.

Think of your company's financial records like a puzzle. The general ledger (GL) is the big picture on the box lid - it's supposed to show you exactly how everything fits together. General ledger reconciliation is the process of making sure all the individual puzzle pieces - your bank statements, sub-ledgers, and other financial documents - actually match that final picture.

It's a crucial health check for your finances. This verification process is your best defense against errors and potential fraud, giving you a financial picture you can actually trust.

Unpacking General Ledger Reconciliation

So, what exactly is the general ledger? It’s the master book of accounts for your business. Every single transaction, from a major equipment purchase down to a box of paper clips, ends up recorded here.

But a master book is only useful if it’s accurate. That’s where general ledger reconciliation steps in. It's the methodical process of comparing the balances in your GL accounts against their supporting documents to make sure everything lines up perfectly. We're not just talking about your bank account; this covers a whole range of financial data.

The Key Players in Reconciliation

Reconciliation isn’t a single action but a series of checks and balances across different parts of your business. You're essentially cross-referencing your GL with independent sources to confirm that the numbers match.

The most common types you'll encounter are:

-

Bank Reconciliation: This is the one most people are familiar with. You're simply matching the cash records in your GL to your official bank statements.

-

Sub-ledger Reconciliation: Here, you verify that a summary account in the GL (like Accounts Receivable) perfectly matches the detailed report from its own sub-ledger.

-

Vendor and Customer Reconciliation: This involves double-checking that the balances you have for specific vendors (Accounts Payable) or customers (Accounts Receivable) align with what their records show.

This whole process is about ensuring the integrity of your financial data. The typical steps involve identifying the accounts to be reconciled, comparing the balances, hunting down any discrepancies, and making the necessary adjustments to fix them.

While a monthly reconciliation is the gold standard for most businesses, the frequency can change. Some smaller companies might do it quarterly, depending on their transaction volume and the risk level of the accounts. You can discover more about this foundational process at Ledge.co.

To make this clearer, let's break down the core components you'll be working with.

Key Components of GL Reconciliation at a Glance

This table breaks down the fundamental elements involved in the reconciliation process, clarifying the purpose of each component for easy understanding.

| Component | Role in Reconciliation | Common Example |

|---|---|---|

| General Ledger (GL) | The central "book of truth" that summarizes all financial transactions. It's the primary record you are verifying. | The main "Cash" account balance. |

| Sub-Ledger | A detailed record of transactions for a specific control account in the GL. It provides the granular detail. | The Accounts Receivable sub-ledger, listing every individual customer invoice. |

| Source Documents | External or independent records used to confirm the accuracy of GL entries. | Bank statements, vendor invoices, credit card statements. |

| Reconciling Items | Discrepancies found during the comparison, which must be investigated and resolved. | A bank service fee recorded on the bank statement but not yet in the GL. |

Understanding these pieces is the first step to mastering the reconciliation workflow and ensuring every number is accounted for.

Why Even a Tiny Mismatch Matters

Imagine you're building a house and the foundation is off by just one inch. It doesn't seem like much at first. But by the time you get to the roof, that tiny error has magnified into a massive, costly structural problem.

Your financial records work the exact same way.

A forgotten bank fee of $25 or a single duplicated invoice might feel trivial at the moment. But if left unchecked, these small errors compound. Over time, they can lead to significant financial misstatements, incorrect tax filings, and terrible business decisions made with faulty data.

Ultimately, the goal is to ensure that the story your general ledger tells is 100% accurate and reliable. It’s the foundation that solid financial management is built on, protecting your business from hidden problems and paving a clear path for growth.

Why Accurate Reconciliation Is a Business Lifesaver

It’s easy to dismiss general ledger reconciliation as just another tedious bookkeeping chore. But that's like calling a smoke detector just a piece of plastic on the ceiling. In reality, both are silent guardians, constantly on the lookout for hidden dangers that could spell disaster. Accurate reconciliation is your financial smoke detector, protecting you from threats like fraud, compliance nightmares, and nasty cash flow surprises.

When you do it right, the process is far more than just ticking and tying numbers. It becomes a powerful strategic tool that ensures your company’s financial foundation is built on solid ground, not shaky assumptions.

Protecting Against Financial Threats

One of the biggest wins from regular reconciliation is its ability to catch fraud and errors before they snowball. Unauthorized transactions, accidental duplicate payments, or even simple data entry typos can be spotted and fixed quickly. Think of it as a high-definition security camera for your company’s finances - it catches suspicious activity that might otherwise go completely unnoticed for months.

For example, a sharp eye on your accounts payable reconciliations might uncover that you’ve been paying the same vendor invoice twice. It’s a surprisingly common mistake that can bleed a company dry over time. Without that routine check, the cash just quietly disappears.

A study by the Association of Certified Fraud Examiners (ACFE) found that organizations using proactive data monitoring - a key part of reconciliation - detected fraud 60% faster and suffered 58% lower losses than those without.

This isn't just about stopping outside threats. It strengthens your internal controls, creating a system where every dollar is tracked and its movement is verified.

Ensuring Compliance and Accurate Reporting

Inaccurate financial statements are a huge liability. They aren't just an internal headache; they can lead to serious legal and regulatory heat. Public companies, for instance, must adhere to strict regulations like the Sarbanes-Oxley (SOX) Act, where accurate reconciliations are a non-negotiable part of maintaining internal controls.

Even if you’re a private business, your lenders, investors, and the tax man all depend on the integrity of your financial reports. A misstated asset or an incorrect liability could torpedo a loan application, scare off potential investors, or trigger a painful audit.

Ultimately, this process makes sure your financial statements paint a true and fair picture of your company’s health. It’s all about creating a reliable financial record, which highlights the importance of the concept of a single source of truth for data.

Gaining True Financial Visibility

Maybe the most important benefit of all is getting a crystal-clear, reliable view of your cash flow and overall financial position. An unreconciled accounts receivable ledger, for example, can be dangerously misleading. It might show impressive revenue figures, but if that cash hasn't actually been collected, you could be heading for a crisis without even knowing it.

Accurate reconciliation gives you the clarity you need to make decisions with confidence.

-

Better Planning: You can build budgets and forecasts based on numbers you actually trust.

-

Smarter Operations: It becomes much easier to spot bottlenecks, like customers who are always late to pay or expense categories that are getting out of hand.

-

Stronger Confidence: When you present clean, well-documented financials, you build trust with investors, lenders, and your own leadership team.

At the end of the day, knowing exactly where your money is and where it’s going is what allows you to steer the ship effectively. It transforms your financial data from a source of anxiety into your most powerful strategic asset.

A Step-by-Step Guide to the Reconciliation Process

Knowing why reconciliation matters is one thing, but actually seeing how it’s done is another. Let’s walk through the general ledger reconciliation process with a practical, step-by-step guide. Think of this as your roadmap to making sure every single number on your books is accurate, verified, and ready for action.

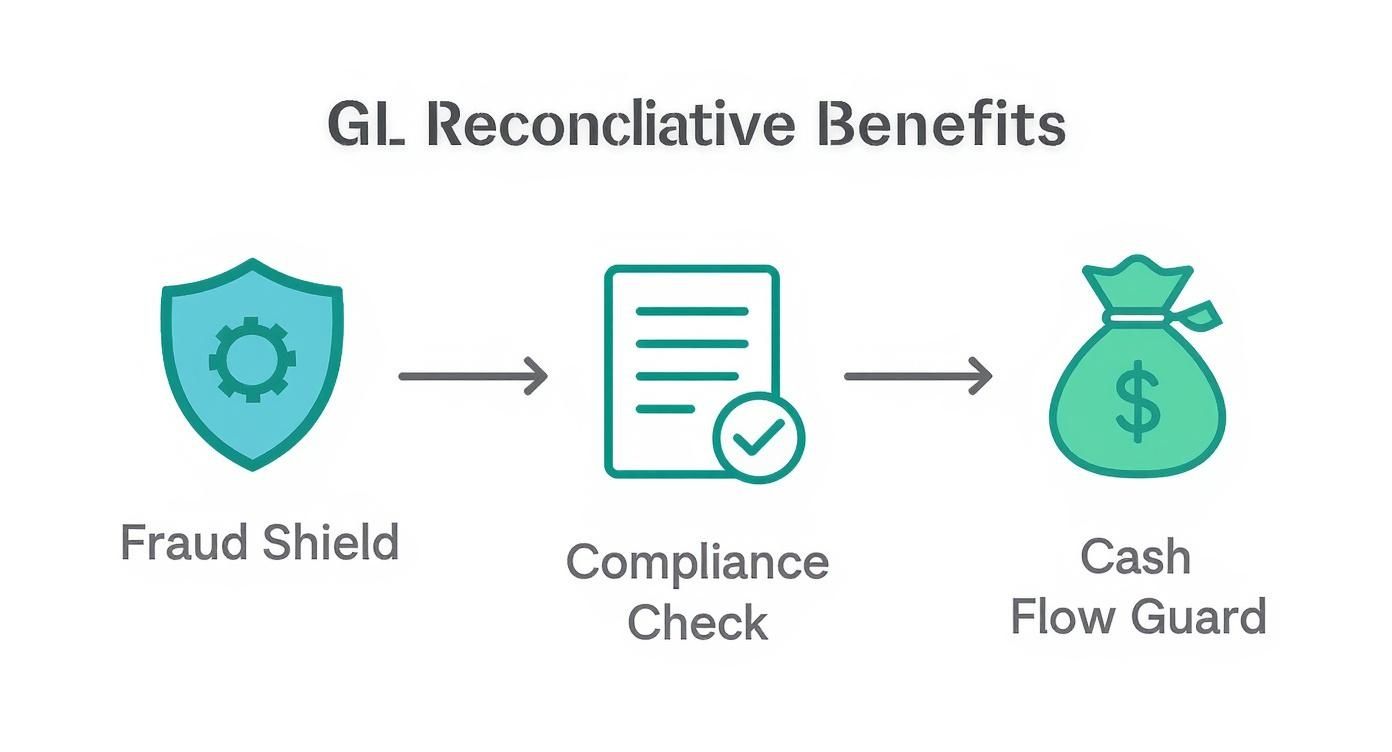

This infographic breaks down the core benefits you unlock with a solid reconciliation process, from catching fraud to getting a better handle on your cash flow.

As you can see, it acts as a multi-layered defense, protecting your company's financial health at every turn.

Step 1: Gather Your Financial Documents

Before you can compare a thing, you need to get all your paperwork in a row. This is the foundation of the entire reconciliation. You're basically gathering the general ledger's side of the story and all the independent source documents that will either back it up or challenge it.

For any given account, you’ll typically need:

-

The General Ledger Account Detail: This is your starting point - a printout or export showing every single transaction that hit the account during the period.

-

Supporting Sub-Ledgers: For big control accounts like Accounts Receivable, you'll need the detailed aging report that breaks down every customer invoice.

-

External Source Documents: Here’s your third-party evidence. This includes things like bank statements, credit card statements, vendor invoices, or loan agreements.

Getting everything organized and ready from the get-go makes the next steps so much smoother. Don't skip this prep work; it’s crucial for an efficient workflow.

Step 2: Compare Balances Line by Line

With all your documents in hand, the real detective work begins. This step involves a meticulous, line-by-line comparison of the transactions in your general ledger against their source documents. You're hunting for perfect matches between your internal records and the external proof.

For example, when reconciling your cash account, you'd match each deposit and withdrawal in your GL with the corresponding entries on the bank statement. The goal is simple: tick off every item that appears on both lists. Anything left unticked on either side is a discrepancy that needs a closer look in the next step.

This comparison phase is where the magic of reconciliation really happens. It’s the active process of verification that turns your financial records from just a list of numbers into a trusted, reliable source of business intelligence.

This step can definitely be tedious, but you can’t overstate its importance. Every single item you match strengthens the integrity of your financial data.

Step 3: Investigate and Identify Discrepancies

It’s incredibly rare for everything to match up perfectly on the first go. This is where you put on your investigator hat and figure out why certain things don't align. These discrepancies, or "reconciling items," are the loose ends you need to tie up.

Some of the usual suspects include:

-

Timing Differences: A classic example is a check you recorded in your GL on the last day of the month that doesn't actually clear the bank until the second day of the next month.

-

Unrecorded Transactions: The bank might hit you with a service fee that you haven't entered into your general ledger yet.

-

Data Entry Errors: A simple typo, like transposing numbers ($54 instead of $45), is a surprisingly frequent culprit.

-

Missing Invoices: You might see a payment on the bank statement, but the vendor invoice it belongs to was never entered into your accounts payable system.

Each mismatch needs to be identified and understood. This isn't just about finding mistakes; it’s about getting a much deeper understanding of your business's financial activity.

Step 4: Make Adjusting Journal Entries

Once you've figured out what caused a discrepancy, it's time to fix it. You do this by creating adjusting journal entries in your general ledger. These entries are what make your internal books accurately reflect reality.

For instance, if you found a $15 bank service fee on your statement that wasn't in your GL, you'd create a journal entry to record that expense. Just like that, your GL's cash balance is brought back into alignment with the bank's records. For more hands-on tips, a good balance sheet reconciliation checklist can be a huge help.

This is the step that formally corrects the errors and omissions you uncovered, making sure your financial statements are spot-on. The time this whole process takes can vary a lot. Benchmarking data shows the median time for GL reconciliation is about six hours, but it can easily stretch to ten hours for more complex businesses. You can learn more about industry reconciliation timeframes from CFO.com.

Step 5: Prepare the Reconciliation Report

The last step is to document all your hard work. A formal reconciliation report summarizes the entire process, proving that the general ledger balance and the source document balance are in agreement after you've accounted for all the reconciling items.

This report is a vital piece of your audit trail. It provides clear, undeniable evidence to managers, auditors, and stakeholders that the account has been properly verified. It’s your proof of diligence and strong internal controls, which ultimately solidifies the trustworthiness of your financial data.

Common Reconciliation Challenges and How to Overcome Them

Even the sharpest accounting teams hit a few snags during general ledger reconciliation. Let's be honest, the process is designed to uncover problems, but sometimes, the process is the problem. Recognizing these common hurdles is the first step to building a smoother workflow that doesn't feel like a dreaded monthly chore.

Most of these headaches come from sticking with old-school, manual methods. A spreadsheet might cut it when you’re just starting out, but as your business grows and transactions pile up, it quickly becomes a major source of frustration and risk.

The Manual Data Entry Bottleneck

The first major culprit? The sheer amount of manual data entry.

When every single invoice, receipt, and bank transaction has to be typed into a system by hand, the door for human error swings wide open. A simple slip of the finger - entering $95 instead of $59 - can send your team down a rabbit hole for hours, hunting for a tiny discrepancy.

It's not just about mistakes; it's a huge time-suck. Your skilled finance pros get stuck doing mind-numbing data entry instead of strategic analysis that actually drives the business forward. It’s a classic bottleneck that slows the entire financial close to a crawl.

The real fix is to minimize manual touchpoints. Tools that capture receipt data or process invoices automatically pull information directly from the source, slashing the risk of typos and giving your team back countless hours every month.

When you take people out of the basic data entry loop, accuracy skyrockets, and so does morale. It’s a win-win.

The Frustration of Missing Transactions

Another all-too-common headache is the endless hunt for missing documents or transactions that were never recorded. A payment hits the bank statement, but where’s the invoice? A vendor calls about a bill you have no record of. Suddenly, your accounting team turns into a group of detectives, digging through emails and shuffling papers.

This chaos is especially bad in companies without a central hub for financial documents. Invoices get sent to random inboxes, paper receipts vanish, and simple communication gaps mean transactions just fall through the cracks. If you're looking to get organized, reviewing some essential bank reconciliation tips is a great place to start building better habits.

The best way to solve this is by creating a single source of truth. Set up a system where all invoices go to one dedicated email address or are captured automatically. This creates a clean, searchable trail that makes finding what you need a simple task, not a frantic investigation.

The Hidden Risks of Spreadsheets

For decades, spreadsheets have been the default tool for reconciliation. They're familiar and flexible, but they come with some serious hidden dangers that can threaten your financial data's integrity. Version control is a nightmare - is everyone really working from the master file, or is someone using a version they saved to their desktop last week?

Worse, spreadsheets have no real audit trail. It’s almost impossible to see who changed what and when, which is a massive red flag for auditors and a security concern. A single broken formula can silently corrupt your entire reconciliation, creating errors that are incredibly difficult to find.

Manual vs Automated Reconciliation Workflows

As your business scales, the cracks in a manual spreadsheet-based system start to show. It becomes slow, clunky, and a genuine liability. Here’s a quick look at how a manual workflow stacks up against an automated one.

| Feature | Manual Reconciliation (Spreadsheets) | Automated Reconciliation (Software) |

|---|---|---|

| Time Investment | Hours or days of manual data entry and matching. | Minutes. Data is imported and matched automatically. |

| Accuracy | Prone to human error (typos, formula mistakes). | High. Reduces human error to nearly zero. |

| Scalability | Becomes slow and unmanageable as volume grows. | Easily handles thousands of transactions. |

| Audit Trail | Lacks a clear, unchangeable record of who did what. | Provides a secure, time-stamped log of all actions. |

| Collaboration | Difficult version control leads to confusion. | Centralized platform ensures everyone is on the same page. |

| Security | Files can be easily altered, deleted, or shared. | Role-based permissions and robust security protocols. |

The takeaway is clear: graduating to a dedicated reconciliation tool isn't just a nice-to-have; it's a necessary step to secure your finances and free your team to do more valuable work.

How Automation Is Changing the Reconciliation Game

Let's be honest - the days of finance teams being buried under mountains of spreadsheets, manually ticking off transactions, are numbered. And that's a good thing. Modern automation isn't just tweaking the general ledger reconciliation process; it's completely overhauling it, turning a tedious, error-prone chore into a smart, strategic part of the business.

Think of it this way: instead of spending hours just confirming what happened yesterday, automation frees up your team to focus on what matters most - analyzing financial data, spotting trends, and helping steer the company toward its next big opportunity. The right tools deliver speed, accuracy, and security that manual processes just can't touch.

The global shift toward these tools is undeniable. This chart from Straits Research paints a clear picture of the account reconciliation software market's growth, showing just how quickly businesses are adopting automation.

This isn't just a minor trend. It's a massive move away from old-school methods toward smarter, more scalable solutions that give finance teams the power to close the books with confidence.

Gain Speed and Pinpoint Accuracy

The first thing you'll notice with automation is the incredible speed. Tasks that used to take days of painstaking work can now be knocked out in minutes. Automated platforms plug directly into your bank feeds, accounting software, and other data sources, pulling in thousands of transactions in the blink of an eye.

But the real magic happens with the matching algorithms. These smart systems instantly compare huge datasets and automatically match the vast majority of your transactions based on rules you set. This doesn't just make things faster; it practically eliminates human error like typos or missed entries, giving you a much more reliable reconciliation.

Imagine you're running an e-commerce store with thousands of daily sales. Automation could:

-

Pull in sales data directly from your storefront.

-

Instantly match every sale to its corresponding deposit from your payment processor.

-

Flag any oddities - like chargebacks or unexpected fees - for you to review.

What was once a logistical nightmare becomes a smooth, almost effortless workflow, keeping your financial records consistently accurate.

Boost Security and Build an Airtight Audit Trail

Beyond speed, automation gives you a level of security and transparency that a spreadsheet could only dream of. Every single click and change made within an automated system is logged, creating a permanent audit trail. It shows exactly who did what and when. Come audit time, this is gold - it’s clear, easily accessible proof of solid internal controls.

Automation turns reconciliation from a backward-looking chore into a real-time health check for your finances. It builds a secure, transparent environment where your data is constantly being verified, not just glanced at once a month.

This shift is part of a much bigger picture. The global market for account reconciliation software was valued at around USD 3.00 billion in 2024 and is expected to skyrocket to USD 10.38 billion by 2033. This boom is fueled by the need for flexible, cloud-based tools that offer real-time insights for today's finance teams.

From Number-Crunching to Strategic Insights

This might be the biggest win of all. When automation handles the repetitive grunt work, your finance experts can finally step into a more strategic role. They can use their time to dig into the exceptions the software flags, analyze spending patterns, and forecast cash flow with far greater precision. This is particularly powerful for complex areas like accounts payable, where dedicated invoice reconciliation software can provide a crystal-clear view of vendor payments.

And the benefits don't stop there. Good automation in one area often bleeds into others. By speeding up your general ledger reconciliation, you also lay the groundwork for overall financial reporting automation, helping you close the books faster and generate reports you can actually trust. When you embrace these tools, you're not just fixing a single accounting headache - you're building a more resilient, forward-thinking finance department.

Best Practices for a Flawless Reconciliation Workflow

Knowing the steps of a general ledger reconciliation is the easy part. The real challenge? Building a process that’s smooth, reliable, and doesn't feel like a mad dash every single month. To get there, you need to adopt a few key habits that will turn this dreaded task into a well-oiled machine.

Think of it like regular maintenance on a car. You don’t wait for the engine to seize up; you change the oil, check the tires, and keep it running clean. These practices do the same for your financial operations, saving you from major breakdowns down the road.

Establish a Consistent Reconciliation Schedule

If you take away only one thing, let it be this: be consistent. Don't let reconciliations pile up until the end of the quarter or - even worse - the end of the year. That’s a recipe for disaster.

Performing reconciliations on a fixed monthly schedule is the gold standard. This rhythm ensures you catch discrepancies or errors quickly, before they snowball into a massive investigative headache. A regular schedule also makes the whole process feel less overwhelming. Instead of staring down a mountain of transactions, your team gets to tackle manageable chunks.

Standardize Your Procedures

Consistency isn't just about when you do it, but how you do it. Every account should be reconciled using the same clear, documented steps. Creating standardized templates and checklists is a game-changer because it means nothing gets missed, no matter who on your team is handling the task.

Why is this so important?

-

Clarity: Everyone on the team knows exactly what to do and which documents they need. No guesswork.

-

Efficiency: Your team can get into a groove and move faster without having to reinvent the process every time.

-

Audit-Readiness: When auditors come knocking, you can hand over clean, consistent documentation. They love that.

By documenting your workflow, you create a single source of truth for how reconciliation should be done. This simple step strengthens your internal controls and makes your financial processes scalable as your business grows.

Implement Segregation of Duties

This one is a non-negotiable for preventing fraud: segregation of duties. In plain English, the person who reconciles an account shouldn't be the same person who manages the transactions in it. For example, the employee who reconciles the bank statement shouldn't also be the one approving payments or depositing cash.

This separation creates a natural system of checks and balances. It makes it incredibly difficult for a sketchy transaction to slip through unnoticed, as it would require two or more people to be in on it. Even if you're running a small business with a lean team, finding creative ways to divide these key financial tasks is critical for protecting your assets.

Got Questions? We've Got Answers

Even with a solid plan in place, it's natural to have a few questions about how general ledger reconciliation works in the real world. Let's dig into some of the most common ones we hear.

How Often Should We Be Reconciling the General Ledger?

The honest answer? It depends on your business. For most companies, a monthly reconciliation is the gold standard. It’s frequent enough to catch issues before they snowball but manageable for most accounting teams.

If you’re running a business with a ton of transactions - think e-commerce or retail - you might want to reconcile critical accounts like cash and sales even more often, maybe weekly or even daily. The absolute minimum for any business should be quarterly, just to keep your financial reports from going completely off the rails.

What's the Difference Between Bank Reconciliation and General Ledger Reconciliation?

This is a fantastic question, and it's a common point of confusion. Think of it like this: bank reconciliation is one slice of a much larger pie, and that pie is the general ledger reconciliation.

-

Bank Reconciliation is laser-focused on one thing: making sure the cash balance in your books matches the cash balance in your bank account. That’s its entire job.

-

General Ledger Reconciliation is the big picture. It’s about verifying all the accounts on your GL by checking them against their source documents - sub-ledgers, loan statements, credit card bills, you name it.

So, while you can't have a healthy GL without reconciling your bank accounts, it’s just one step in the full process.

Can We Just Use Spreadsheets for This Instead of Software?

You certainly can, and many small businesses start out this way. Spreadsheets are familiar, and the cost is right (free!). For a business with just a handful of transactions, they can get the job done.

But as you grow, spreadsheets quickly turn from a simple tool into a major liability. They're a breeding ground for human error - typos, busted formulas, copy-paste mistakes - and they offer zero security or a clear audit trail. Collaboration becomes a mess of "final_v2_final_final.xlsx."

This is where dedicated software comes in. It automates the tedious work of importing data, instantly flags things that don't match up, and creates a clean, permanent record of your work. The time saved and errors avoided make it a no-brainer for any business looking to scale.

Ready to stop wrestling with spreadsheets and secure your reconciliation process? With Tailride, you can automatically pull invoices and receipts right from your email, match transactions in a snap, and build an audit-proof workflow. See how much easier finance can be at https://tailride.so.